Credit for real estate owners: Apply for a favorable owner loan with top interest rates

You are the owner of one or more properties and would like to take out a loan at fair and attractive conditions? Do you plan to modernize or refit your property(ies), or do you need funds for something completely different that has nothing to do with your properties? Then your first thought will probably be to visit your local bank and ask about the conditions and requirements for a loan. With this you are actually well advised, because as a real estate owner you have optimal chances to get a good loan from banks – not only because your real estate is an ideal factual loan collateral, but also because your house bank most likely already knows you because of your real estate financing.

So, as a real estate owner, you are one of the privileged "favorite customers" of a bank, which of course makes the whole thing quite easy for you. Nevertheless, it's worth looking into how you can get the best conditions and most favorable interest rates.

Loan for property owners from your own house bank or another German branch bank

Your first port of call for a loan application is your local bank. You probably have a contact there, your personal account manager, who has already guided you through the process of financing your property(ies). Maybe you're also still paying off a real estate loan at your local bank. Now, however, you do not want to buy a new property, you need the installment loan for something else. What about the requirements you need to meet?

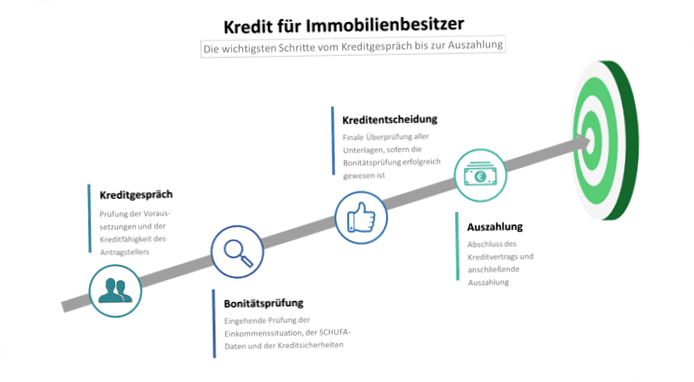

Conditions for approval of an installment loan for real estate owners

Regardless of whether they are property owners or not, all loan applicants to German banks must meet the same requirements. If nothing has changed since your last credit approval in the course of real estate financing, you can assume that you meet the general requirements.

- Age of majority

- Residence in Germany

- Current account with a German bank

- Existing, regular income

Income check: Do the income conditions allow for a loan approval??

Before banks approve a loan, they always carry out a thorough income check. The best chances of obtaining a loan are those property owners with a regular and good income. Income from rentals also counts as income, so you have all the better chances if one or more of your properties are rented out.

If you can then also show an income as an employee or self-employed person, your loan is as good as secure – and even, with a little luck, at better conditions than some other borrowers. Because property owners, even without additional income from rental income, have a good reputation as disciplined savers who always keep track of their finances. The purchase of a home is usually associated with farsightedness and financial forward planning.

Credit assessment: Assessment of payment behavior by SCHUFA

The bank to which the loan application has been submitted, checks not only the income of the applicant, but also his creditworthiness, also called credit rating. The most important element in assessing creditworthiness is the SCHUFA score.

Every person who performs actions of a financial nature in Germany has an entry with the credit agency SCHUFA. Even the opening of a current account or the conclusion of a cell phone contract leads to data being deposited with SCHUFA.

Since the SCHUFA is there specifically to be able to assess the creditworthiness of a person, your house bank has access to this data and it is the entries mainly about payment history and compliance with contract content. Negative entries, which consist for example of unpaid bills, repeatedly received reminders or a private insolvency, affect the credit rating very much.

From the various stored data results in a value, the already mentioned SCHUFA Score. It is a number between 0 and 100, which indicates the creditworthiness in percent.

Do you want to know what the SCHUFA has stored about you? Once a year, every person whose data is stored has the right to receive a copy of all data free of charge, which is not to be confused with the credit report, which is subject to a fee.

Possible collateral for a loan for real estate owners

Banks are interested in potential loan collateral, i.e. possibilities to get the approved money back even if the borrower is no longer able to repay the loan. There are two types of loan collateral: The personal and material loan collateral.

The personal credit security

The classical personal credit security is the guarantee. A person agrees to take on the loan debt if the borrower becomes insolvent. An alternative to this is the co-applicant, who signs the loan agreement together with the property owner and is jointly responsible for repayment from the outset.

The material credit security

When it comes to providing the bank with factual loan collateral, a real estate owner has it very easy, because he has at least one thing of immense value for sure: his property. The bank, in order to secure the loan, is granted a lien on the property by means of a mortgage or a land charge. This not only increases the chances of credit approval, but also the conditions, primarily the interest rate, are thereby usually significantly better.

credit for real estate owners and owner loans without SCHUFA

Real estate owners are usually not among the applicants whose loan requests are rejected by the bank. Nevertheless, you may want to avoid a query of your SCHUFA data or a new SCHUFA entry, which would be unavoidable by a credit approval in any case, for different reasons. In such cases there is a possibility to turn to foreign banks, because only German banks are among the contractual partners of SCHUFA.

Banks from Liechtenstein and especially Switzerland are known for granting loans to foreigners from Germany. That is why the term "Swiss loan" has now even become established.

Income checks and collateral for Swiss loans

However, just because the SCHUFA score is not a factor for Swiss and Liechtenstein banks, it does not mean that they grant loans to real estate owners or owner-occupied loans frivolously. An income check is nevertheless carried out, and credit approval is often linked to certain conditions, for example a permanent employment contract.

In order to increase the chances for an approval, personal or material securities of the credit can be offered also to Swiss or Liechtenstein banks.

Beware of pre-cost claims on loans without SCHUFA

You can recognize professional foreign banks by the fact that you do not have to pay any fees for the credit check. There are however offerers, who require such Vorkosten, and the paid money is lost, if the credit request is rejected then. Waive best completely on loans for real estate owners or owner loans with pre-costs! Lenders who offer such a thing are almost always dubious!

Credit for real estate owners and owner loans from private individuals

Not only banks grant loans, but also private persons can act as lenders. If you find someone in your personal environment who is wealthy enough to grant a loan, this is of course a very advantageous – if at second glance also tense – situation. Alternatively, strangers offer online lending services.

Credit for real estate owners from private individuals from their own environment

The personal loan from an acquaintance, relative or other close person usually has a serious advantage: it is completely or almost interest-free. However, it also has a disadvantage that is at least as serious: Here financial things are brought into a personal relationship and such things unfortunately not infrequently go wrong in interpersonal terms. There may be disputes and a complete rift, for example, if an inability to repay occurs.

That's why it's important to always contract private loans for property owners as well. The contract should be detailed, all the details should be written in it, so that misunderstandings later can not even occur.

Credit for real estate owners from third-party private lenders

There are online platforms where private individuals offer loans. They do this in order to earn money on interest. Many of these providers are professional and honest and offer some people, who do not get money through common channels such as the house bank and the family, a conceivable alternative.

The interest rates, however, are often very high, much higher than with house banks, and therefore almost all property owners are better advised to rather ask their bank or their environment for a loan!

Purposes of credit for real estate owners

Real estate owners can, like other people, take out uncommitted consumer loans, which they can use for a purpose freely chosen by them. These are the classic installment loans. However, there are also some loans that are specifically intended for property owners and are earmarked for a specific purpose. They are called owner loans and offer many advantages to the borrower.

The owner loan

The owner loan, also called housing loan, is specifically and exclusively for purposes related to the property. The money can be used for example

- for renovation and repair

- for modernization and renovation

- for the purchase of furnishings such as furniture and kitchens

- for the construction or extension of gardens and conservatories

- For home improvements, such as converting the attic into living space

For the first two points, some banks give an even narrower loan, the modernization loan.

Owner loans approve most banks for an amount of up to 50.000 euros, the interest rates are usually very favorable at one to two percent. Why the interest rates are so low is easily explained: First, the property owner enjoys the confidence of the bank, because through his property his credit rating is also good. If necessary – if it comes nevertheless to the insolvency – the real estate serves as a material credit security.

Secondly, the money is used for an optimization of the property, and since its value increases, the security for the bank also increases at the same time.

In addition to the favorable interest rates, the housing loan has other customer-friendly features. For example, no land register entry is necessary, which automatically leads to cost savings: Neither the notary has to be paid, nor the entry itself. The loan term and the amount of the installments may choose the borrower himself and then but rely on stability. The rates are no longer adjusted.

Some banks also grant a free special repayment right and the possibility to pause the installment payment for a while. In general, the owner loan is one of the least bureaucratically complex and quickly available loans.

Clarify with your bank if you have to specify exactly what you are using the money for or if you are free to use it as long as you use it only for your property. Because banks handle it differently: some specify a purpose in advance, others give the borrower a free hand.

KREDIT 123 summarizes: Our conclusion on the subject of credit for real estate owners and owner loans

Real estate owners are a privileged group among borrowers. They already have a high credit rating thanks to their real estate, and are also usually considered organized and reliable. To get a credit from the house bank – all the same whether purpose-unbound consumer credit or purpose-bound owner loan – is usually no problem. Especially with home loans, owners also benefit from very customer-friendly conditions and favorable interest rates.

Although a loan from your local bank will be approved in almost all cases, property owners also have other options. If they want to avoid a SCHUFA entry or access to their data stored at SCHUFA, it is worthwhile to apply for a loan from banks in Switzerland or Liechtenstein.

Also private persons – both such from the circle of acquaintances, as well as strangers – offer themselves as lenders. It is important to always draw up a credit agreement – even and especially with private individuals from one's own family or circle of acquaintances.

Comparison between providers: Where to find the best loan for real estate owners?

How high is the interest rate, is there a document requirement for individual uses, is free unscheduled repayment allowed?? There are many questions you need to ask yourself as a property owner when choosing the right lender for you.

The team of KREDIT 123 advises very much to accomplish detailed credit comparisons and to take for it also really time. In addition, property owners are in a very good negotiating position. It is worthwhile to gather the best conditions and request them from the house bank!